But here’s the uncomfortable truth:

Table of Contents

ToggleHere are 5 Reasons to reconsider getting a loan in 2026.

Consider these 5 Reasons before making your decision to get a loan.

The fastest loan is rarely the cheapest loan. Discover the 5 Reasons why.

These 5 Reasons will help you see the bigger picture.

As someone working closely with the CSC Loan Bazar ecosystem, I’ve seen thousands of profiles. Some borrowers saved significantly just by comparing properly. Others paid more for years simply because they trusted the first offer they saw.

Here are 5 Reasons that illustrate the importance of careful selection.

Don’t Take a Loan If You Haven’t Compared Multiple Lenders

Banks promote their own loan.

Apps promote their own loan.

No lender promotes their competitor’s cheaper offer.

When you visit a single bank’s website, you are seeing only one side of the market.

But in reality:

Interest rates vary across lenders.

Approval logic differs.

Some banks favor salaried profiles.

Others prefer self-employed.

Some give longer tenure.

Some offer lower EMI structure.

Without comparison, you are not choosing the best loan —

You are choosing the only loan shown to you.

Smart borrowers don’t apply blindly. They compare.

That’s exactly why structured portals that check multiple institutions through a single profile review often help borrowers see what an individual bank website will never show.

Let’s explore 5 Reasons why understanding the market is crucial.

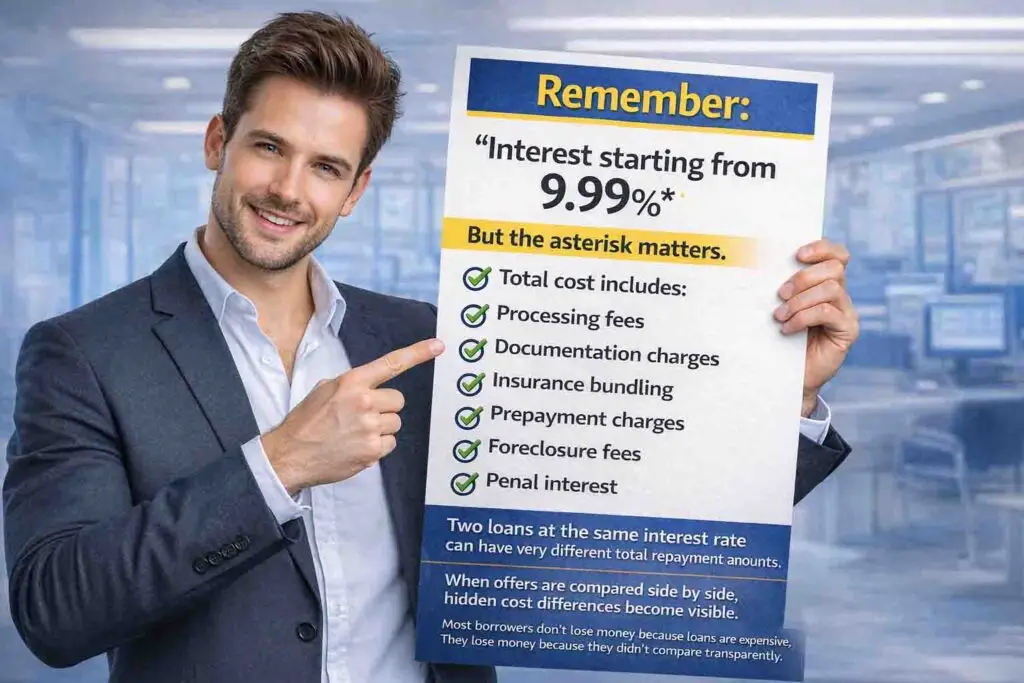

Don’t Borrow If You Don’t Understand the Real Cost

Most websites highlight:

But the asterisk matters.

Total cost includes:

Processing fees

Documentation charges

Insurance bundling

Prepayment charges

Foreclosure fees

Penal interest

Two loans at the same interest rate can have very different total repayment amounts.

When offers are compared side by side, hidden cost differences become visible.

Most borrowers don’t lose money because loans are expensive.

They lose money because they didn’t compare transparently.

That’s why structured evaluation often saves more than impulsive applications.

These 5 Reasons highlight the hidden costs of borrowing.

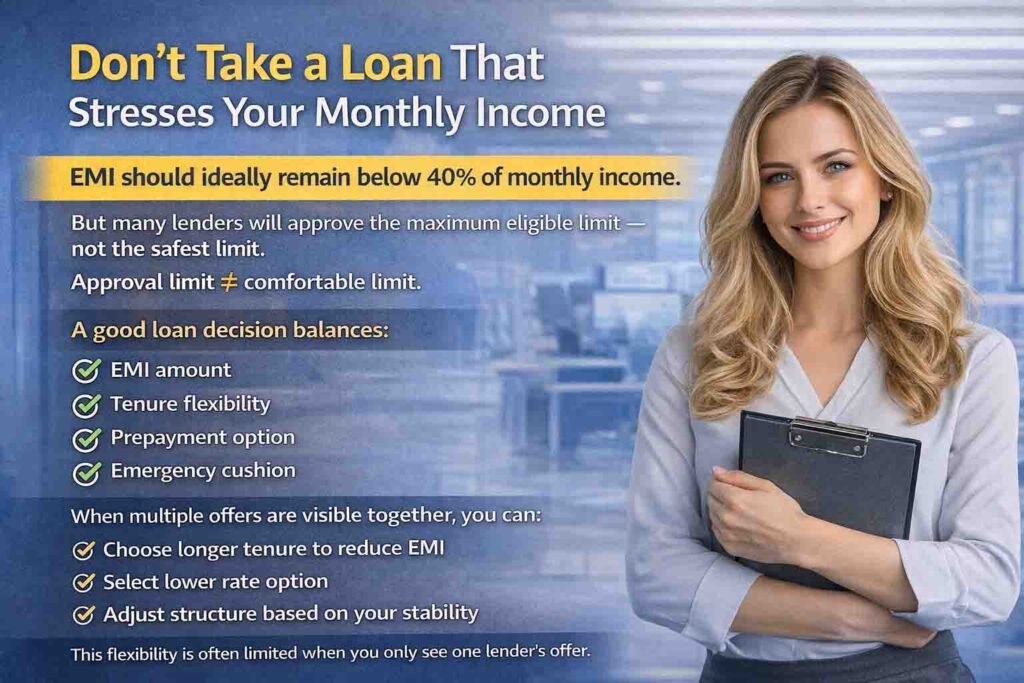

Don’t Take a Loan That Stresses Your Monthly Income - 5 Reasons

EMI should ideally remain below 40% of monthly income.

But many lenders will approve the maximum eligible limit — not the safest limit.

Approval limit ≠ comfortable limit.

A good loan decision balances:

EMI amount

Tenure flexibility

Prepayment option

Emergency cushion

When multiple offers are visible together, you can:

Choose longer tenure to reduce EMI

Select lower rate option

Adjust structure based on your stability

This flexibility is often limited when you only see one lender’s offer.

Here are 5 Reasons to ensure your monthly payments are manageable.

Don’t Apply Repeatedly on Different Apps

These 5 Reasons explain why repeated applications can hurt your score.

Every time you apply randomly:

Your CIBIL may get checked.

Multiple hard inquiries can reduce your score.

Rejections make future approvals harder.

Many people apply at 4–5 loan apps in a week hoping for approval.

That damages credibility.

Instead, eligibility should be matched first.

Filtered applications improve approval probability.

When your profile is evaluated carefully before submission — instead of being sprayed across lenders — your financial reputation stays stronger.

This is something most direct platforms don’t guide you on.

Don’t Take a Loan Just Because It’s “Instant”

Speed is attractive.

But faster approval often means:

Standardized pricing

Limited negotiation

Less profile assessment

Higher default risk margins

Banks and NBFCs price loans based on risk.

If your profile qualifies for better pricing somewhere else — but you never check — you may overpay for years.

Taking a few extra hours to compare can reduce your cost significantly over the tenure.

Instant gratification is emotional.

Low interest is mathematical.

Always choose mathematics over emotion.

Consider these 5 Reasons before opting for instant loans.

The Real Difference Isn’t Bank vs Loan — It’s Single Offer vs Multiple Offers

Understanding these 5 Reasons will make you a smarter borrower.

When you apply directly at a bank:

You get their product.

You accept their pricing.

You see their tenure structure.

But the lending market has 500+ banks, NBFCs, and financial institutions.

Each one evaluates:

Income differently

Business profiles differently

CIBIL scores differently

Existing EMIs differently

What one lender rejects, another may approve comfortably.

What one lender prices at 14%, another may offer at 11–12% depending on profile matching.

That difference across years of repayment matters.

Why Structured Loan Evaluation Matters

Here are 5 Reasons why structured evaluation is essential.

Instead of applying blindly, a smarter approach is:

Compare multiple providers

Understand total repayment cost

Review tenure options

Avoid unnecessary CIBIL impact

Apply selectively

Through gothriwiz.in, integrated with the CSC Loan Bazar system, applicants can explore offers from a wide network of lenders in one structured flow.

Rather than selling one product, the focus is on:

Profile matching

Offer comparison

Cost transparency

EMI suitability

There is a small consultation and service fee of ₹99 + GST.

But consider this:

If structured comparison saves even 1% in interest on a ₹3 lakh loan, the long-term savings can easily exceed that service cost many times over.

The goal isn’t to “push a loan.”

It’s to help borrowers avoid expensive decisions.

When Should You Actually Take a Loan?

You should take a loan when:

It improves your earning capacity

It builds assets

It solves urgent financial stress

EMI is manageable

Cost is optimized

But optimization is the key word.

Loans are tools.

A tool can build a house —

Or create damage.

The difference lies in how carefully it is selected.

Take into account these 5 Reasons for successful borrowing.

Final Thought: Don’t Ask “Where Can I Get a Loan?”

Explore these 5 Reasons before asking ‘Where Can I Get a Loan?’

Ask:

Where can I compare safely?

Where can I see multiple lenders offers?

Where can I reduce overpaying?

Where is my profile evaluated properly?

Because financial mistakes are rarely about borrowing.

They are about borrowing without comparison.

If you decide that you truly need a loan, make sure it’s chosen wisely, evaluated properly, and structured intelligently.

And when you’re ready to explore your options in a more informed and comparative way, you can review offers through gothriwiz.in — where structured comparison, multiple provider visibility, and guided evaluation aim to help you make a confident financial decision.

A good loan doesn’t begin with speed.

It begins with clarity.